Introduction

Payment-in-Kind (PIK) interest is a specialized financing mechanism often used in syndicated loans, mezzanine debt, and private credit markets. Rather than requiring periodic cash interest payments, PIK structures allow the borrower to defer interest by capitalizing it—adding it to the principal balance of the loan. While this can provide strategic flexibility during capital-intensive ramp-up phases or financial distress, it also introduces heightened complexity and risk for both borrowers and lenders.

Understanding the purpose, mechanics, documentation, and operational implications of PIK interest is essential for professionals across finance, legal, operations, and credit risk functions. This guide offers a clear and comprehensive overview designed to educate readers on the foundational concepts, practical scenarios, structural variations, and system and covenant impacts of PIK interest.

Whether you’re structuring a new syndicated loan, reviewing amendments, monitoring risk, or ensuring back-office systems are properly configured, this guide will walk you through the nuances of PIK structures in a digestible and actionable format.

Table of Contents

- What Is Payment-in-Kind (PIK) Interest?

- Definition and Key Terminology

- Capitalized vs Cash Interest

- Why PIK Is Used

- Growth & Ramp-Up Scenarios

- Restructuring & Distressed Situations

- Toggle and Hybrid Structures

- How PIK Works in Syndicated Loans

- Accrual and Capitalization Mechanics

- Cumulative vs Non-Cumulative Interest

- Example Loan Calculations

- Documentation Standards and Legal Framework

- LMA and LSTA Guidelines

- Key Clauses in Term Sheets and Credit Agreements

- Triggers and Toggle Mechanisms

- Operational Considerations and System Challenges

- Loan Servicing and Accounting Complexity

- Dynamic Principal Tracking

- Reporting, Cash Flow Forecasting, and Amortization

- Risk Management and Credit Implications

- Refinancing and Balloon Risk

- Moral Hazard and Credit Monitoring

- Covenant Impacts and Red Flags

- Accounting and Tax Treatment

- GAAP, IFRS, and Tax Jurisdiction Nuances

- Original Issue Discount (OID) and Taxable Income

- Implications for Lenders and Borrowers

- Market Examples and Case Scenarios

- Project Finance Use Cases

- Venture & Growth Debt

- Distress Amendments and PIK-forbearance

- PIK as a Signal: Healthy Tool or Warning Sign?

- Assessing When PIK Makes Sense

- Key Questions for Stakeholders

- Framework for Evaluating PIK Deals

- Best Practices and Takeaways

- Drafting Tips and Common Pitfalls

- Covenant Definitions and Control Points

- Ensuring Operational Readiness and Reporting Integrity

1. What is PIK / Capitalised Interest

Definition

- “Payment‑in‑Kind” (PIK), also called capitalised interest, is a feature in some loan/facility agreements under which interest (or part of interest) is not paid in cash when due, but instead is added (“capitalised”) to the loan’s principal. (Practical Law)

- Over time the outstanding principal grows because of this accrual of interest, and future interest is then calculated on the increased principal (depending on whether the PIK is cumulative or non‐cumulative). (Thompson Coburn LLP)

Key distinctions / terminology

| Term | Meaning / Variation |

|---|---|

| Full PIK | All interest is capitalised (i.e. none is paid in cash during the PIK period). (Thompson Coburn LLP) |

| Split PIK / Partial PIK | Only part of the interest is PIK; the rest is cash interest. |

| Toggle PIK / Pay‑as‑you‑can PIK | The borrower or under certain conditions can choose (or is required) to switch between cash payments and PIK or some mix. Sometimes subject to triggers. (Thompson Coburn LLP) |

| Cumulative vs non‐cumulative interest | In cumulative PIK, interest capitalises, and future interest accrues on the increased principal; in non‐cumulative PIK, sometimes the principal is increased, but interest for subsequent periods may still be based on original principal or some base. (Though non‑cumulative PIK seems less common in syndicated loan markets; many PIK interest provisions imply compounding.) I personally like to call the non-cumulative interest – PIK on Principal Only and this is the name I gave it when I designed and built this feature in Advent Geneva. |

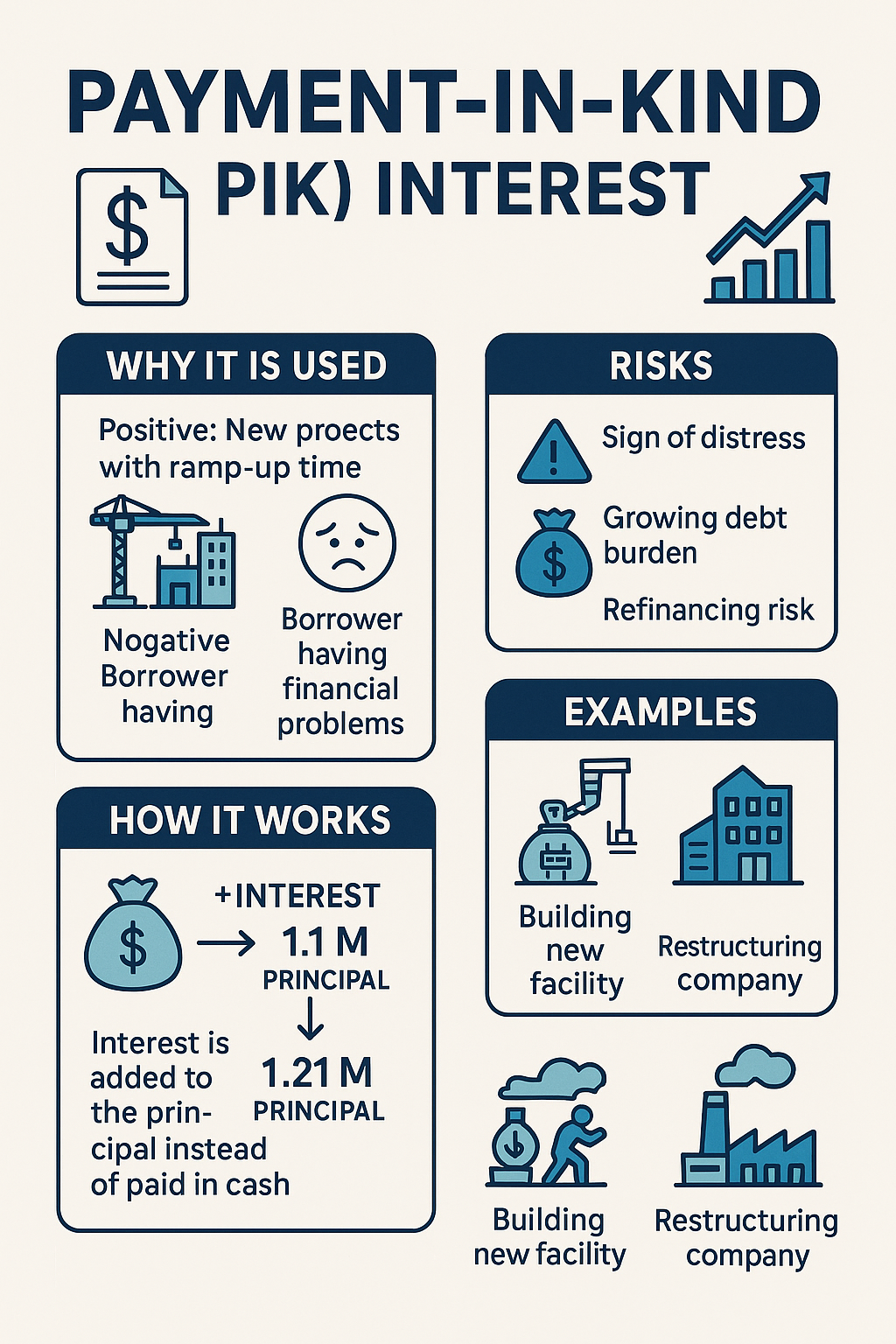

2. Why PIK is Used: Positive / Growth / Ramp vs Distress / Restructuring

PIK is not always a sign of distress—many situations make PIK attractive or even necessary from a financing perspective.

Positive / Growth / Ramp‑up Scenarios

- New large projects that require extensive capital expenditures (CapEx) before revenues ramp up. e.g. infrastructure projects (power plants, pipelines, renewables, mining), real estate development, large industrial equipment. During construction or development phases there may be no or minimal cash flow, so cash interest payments could be very burdensome or even impossible. PIK interest allows borrower to defer cash outflows until project begins producing revenue.

- Venture / growth companies (less mature businesses) or startups where preserving cash runway is critical. They may negotiate PIK interest (or split/toggle PIK) so cash can be used for operations, R&D, sales expansion, etc.

- Seasonal or cyclic businesses where cash flows fluctuate. In off‑season, or early in cycle, borrower may prefer PIK; when cash flows are strong, cash interest may resume.

Negative / Distress / Recovery / Restructuring Scenarios

- A borrower whose cash flow has been negatively impacted (market downturn, loss of contract, cost overrun) may seek or negotiate PIK features as part of amendments to avoid immediate cash interest payments that might push toward default.

- In restructuring or turnaround settings, lenders may allow a PIK period to give breathing room while operations are improved or other financing / asset sales occur.

- Lenders may impose PIK (or change to PIK interest) as a “last resort” or as part of restructuring covenant packages. It’s a warning sign: if a borrower is forced into PIK, that often indicates strain.

3. How PIK Works: Mechanics & Variations

To include PIK interest in a syndicated (term) loan, documentation must define:

- The interest rate(s) applicable during PIK periods (often higher than for cash interest, or includes a premium for PIK). (Thompson Coburn LLP)

- The period(s) during which PIK is permitted or mandatory. Could be early (“ramp‑up”) period; part of a larger facility schedule; or tied to performance/financial metrics.

- Trigger events for switching from PIK back to cash interest (or vice versa). These can be positive triggers (e.g. achieving certain revenue, cashflow, EBITDA, etc.) or negative triggers (e.g. failing cash balance thresholds). (Thompson Coburn LLP)

- Whether PIK interest is cumulative compounding or only capitalised once per period without effect on future interest beyond increased principal (depending on how interest is calculated).

- How (and when) the additional interest is capitalised / added to the principal (e.g. at end of interest period, quarterly, etc.).

- What happens at maturity or refinancing: accumulated PIK interest becomes due (with possibly principal repayments) and may influence refinancing risk since the debt burden has grown.

Example:

- A company takes a $100 million term loan at interest rate “SOFR + 500bps, with PIK interest for the first two years (full PIK), thereafter cash interest.”

- Year 1: interest accrues ≈ $100m * rate, is added to principal → new principal ~$108‑110 million (depending on spread).

- Year 2: same calculation on higher principal, further increase.

- Year 3: cash interest payments begin on the enlarged principal (unless some reduction or covenant requires principal step‑downs).

Another variation:

- A toggle PIK: borrower may elect PIK vs cash, or must do PIK if cash flow insufficient. The PIK version may require paying a premium spread (e.g. +50bps over base interest rate) because the lender takes more risk. (Latham & Watkins)

4. Documentation and Legal / Market Standards (LMA, LSTA etc.)

LMA (Loan Market Association, EMEA etc.)

- LMA standard forms / guides include standard clauses for capitalised interest / payment in kind interest in term loans. These are often part of leveraged finance or mezzanine debt structures. (Practical Law)

- In LMA drafting, clear definitions of “capitalised interest”, when it is to be capitalised, whether interest accrues on the increased principal etc., are essential. Ambiguities can lead to disputes.

LSTA (Loan Syndications & Trading Association, U.S.)

- LSTA documentation, trading forms, secondary market confirmations assume certain conventions around PIK interest. For example, in LSTA’s secondary trading confirmations, there are provisions for how “PIK Interest” is allocated in purchase price calculations: PIK interest capitalised before Trade Date, PIK interest capitalised or accrued after Trade Date, etc. (SEC)

- PIK generally trades free, which means that the full PIK amount goes to the buyer and no delayed compensation is exchanged.

- In U.S. credit / private debt deals, PIK interest is increasingly seen (especially in direct lending, private credit) and legal practices have evolved to include split or toggle PIK, more performance triggers. (Thompson Coburn LLP)

5. Operational, Accounting, and Risk Management Challenges

PIK introduces many complexities. In operations, accounting, risk management, legal, etc.

Operational / Systems Challenges

- Tracking of increasing principal: systems must support dynamic principal balances; interest accruals, compounding; schedule adjustments.

- Interest calculation: must know exactly which rate applies, whether interest computed on original or updated principal; timing of capitalisation.

- Cash flow modelling and forecasting: because cash interest payments may be zero for PIK periods, forecasting of debt service obligations must account for “balloon” of accumulated PIK interest.

- Amortization / principal repayment scheduling: often PIK loan are bullet repayment (no amortization), or have minimal amortization; systems must flag matured or due accumulated obligations.

- Covenants: financial covenants often reference debt service, leverage, interest cover, which need cash interest payments. PIK interest may or may not count in definitions; you must know how “interest expense”, “finance charges”, “debt service” are defined. Also, PIK may complicate or violate certain covenants or trigger defaults.

Accounting & Tax

- For the borrower (and investor / lender), PIK interest generally means interest expense is recognized even when cash not paid, because the interest accrues. However, whether compounding is allowed for accounting recognition depends on local GAAP / IFRS / U.S. GAAP.

- Balance sheet implications: liability increases; cash flow statements: less outflow in operating or financing until actual cash payment.

- Tax treatment: PIK interest may raise issues around Original Issue Discount (OID) rules, contingent interest, taxable income for lenders even if cash isn’t received (in some jurisdictions). (Latham & Watkins)

Credit / Risk

- Higher risk to lenders: the principal grows, making repayment more onerous; possibility of borrower being unable to refinance or pay at maturity.

- Potential for mis‑alignment of incentives: borrower may prefer PIK to preserve cash even when paying cash might be preferable in long‑term value (but that’s part of negotiation).

- Monitoring risk: need to monitor triggers, performance, liquidity, cash flow; need visibility into operational and financial metrics.

6. When PIK May Be a Warning Sign vs Normal Part of Structure

Because PIK can be used in healthy growth projects, but also in distress, it’s important to distinguish.

| Signal | More likely a “normal / expected” PIK situation | More likely a warning / distress signal |

|---|---|---|

| Project or investment with long ramp-up time / large capex front‑loaded | ✔ | — |

| Borrower has strong sponsor, credible business plan, ability to project revenues in near‑future | ✔ | — |

| PIK only for limited, agreed period; with triggers back to cash pay; rates premium set appropriately | ✔ | — |

| PIK is part of leveraged finance / mezzanine financing, expected in the risk level | ✔ | — |

| Borrower requests PIK or toggle PIK due to unexpected cash flow shortfall; PIK beyond initial period; triggers moving | — | ✔ |

| PIK interest used repeatedly, extended, or principal has ballooned, making refinancing risky | — | ✔ |

| Covenants are failing, liquidity is tight, and PIK is one concession among many (restructuring, etc.) | — | ✔ |

7. Best Practices / Key Questions in Structuring PIK

When drafting, negotiating or reviewing PIK provisions, or managing loans with PIK interest, asking these questions helps ensure clarity and risk control.

- How is PIK interest defined in the agreement?

- Is it clearly “capitalised interest” or “interest added to principal”?

- How often is interest capitalised (monthly, quarterly, annually, at end of period)?

- Is interest calculated on increased principal (i.e. compounding)?

- If cumulative compounding, growth of debt can be exponential.

- If non‑cumulative, interest may remain fixed base even as principal increases.

- What interest rate / spread applies for PIK vs cash pay?

- Is there a premium for choosing PIK?

- What periods / triggers allow (or force) PIK?

- Are there automatic periods (e.g. first n years)?

- Are there triggers based on performance (cashflow, EBITDA, revenue, liquidity)?

- Is PIK toggle discretionary or mandatory under certain conditions?

- What are the covenants’ definitions of interest, debt, debt service, finance charges, etc.?

- Does “interest expense” include accruals? Does “debt service” include cash interest only, or PIK?

- Maturity / refinancing risk

- Will the borrower be able to refinance or repay the enlarged principal?

- Is there a “step‑down” or amortization scheduling?

- Accounting & tax implications

- For borrower, for lenders: tax deductions, interest income, OID, contingent interest etc.

- Jurisdictional issues: Some laws limit capitalization of interest or compound interest.

- Operational system readiness

- Loan servicing systems must support increasing principal, compounding, switching interest modes, etc.

- Reporting to lenders, agents, investors must reflect the true debt burden.

- Disclosure to lenders and market

- Clear term sheets, clear documentation; in syndicated loans, all lenders need to understand what they are committing to.

- For secondary market trading: how PIK interest will be treated in assignments, trade confirmations, purchase price. (LSTA has standard language here.)

8. Example Scenarios (Illustrative)

Scenario A: A new renewable energy project

- Borrower builds large solar farm. Construction 2 years before commissioning. No revenue for first year, small in second year.

- Loan: $200 million. Interest rate cash‑pay after Year 2; first 2 years, full PIK interest. Then start cash interest. Principal is bullet at Year 10.

- Effect: At end of Year 2, principal may have grown by both years of PIK, so Year 3 interest payments are higher; borrower must plan accordingly.

Scenario B: Growth startup / venture debt

- Borrower with promising tech product, but sales still small. Needs cash to hire, build sales pipeline. Lender agrees to split PIK: 50% cash, 50% PIK for first 18 months; then 100% cash. Cash interest rate maybe lower; PIK portion has premium spread. There might be a trigger: if revenue reaches X or ARR > Y, borrower must pay more in cash.

Scenario C: Distress / restructuring

- A company’s revenues fall due to demand shock. Cashflow insufficient to cover interest payments. Lenders agree to amend the facility; change interest from cash pay to full PIK for 1 year, then cash pay schedule resumed. Debt burden grows; but helps avoid default, give time for stabilisation.

9. Legal / Regulatory / Market Risks and Pitfalls

- Enforceability of PIK interest / compounding: In some jurisdictions, laws on usury, maximum interest, or rules against compound interest may limit or invalidate certain PIK clauses.

- Ambiguity in documentation: If definitions (interest period, calculation, capitalisation) are vague, disputes may arise: over when interest is added to principal; whether interest for next period uses old or new principal; whether PIK interest counts as “interest expense”, etc.

- Refinancing risk / “balloon risk”: Because principal increases, at maturity borrower may be faced with a large debt that may be hard to pay off or refinance, especially if cashflows did not grow as projected.

- Investor / lender perception / pricing risk: Lenders may require higher spreads, or demand stricter covenants if PIK is part of deal; otherwise moral hazard.

- Credit rating / credit agencies might view PIK as a negative: If PIK is being used because of cash flow stress, may impact ratings.

- Accounting / tax surprises: Tax authorities may treat accrued interest differently; lenders might have taxable income while not receiving cash; original issue discount; contingent interest complications.

10. Summary / Key Takeaways

- PIK interest is a tool that gives borrower flexibility, especially in early / ramp‑up phases, or when preserving cash is essential.

- But it comes at cost: growing principal, compounding risk, refinancing risk.

- Structuring must be precise: clarity in rate, period, triggers, definition of interest, how and when capitalisation happens.

- Legal, accounting, operational systems must be ready.

- In healthy projects, used properly, PIK is valuable; in distressed situations it can be a useful lifeline—but often a signal that things have gone off‑plan if used beyond what was originally agreed.

Training prepared and provided by:

Gage Gorman

www.gagegorman.com

(Thank you Mimi, for inspiring this guide)